.png)

Self-funding you company’s healthcare plan has a lot of upsides, including more flexibility, happier, healthier employees, and big potential savings. But one thing that can give businesses pause when they consider making the switch is the underlying financial risk. By taking on the responsibility to fund your employees’ healthcare, you’re ultimately putting yourself on the hook for all the claims that arise when your employees use their healthcare benefits. And as everyone knows, health and healthcare can be very unpredictable—just one member getting diagnosed with a chronic disease, for example, could mean expensive ongoing treatment that increases care claims significantly.

Key Stop-Loss Terms

Now that we’ve walked through the basics, it’s time to dive into the complexity. Here are the key terms and concepts you need to know to get the full picture of how stop-loss works.

Specific coverage vs. aggregate coverage

These terns refer to how deductibles and spending limits are set in your stop-loss contract. Contracts can include one or both kinds of coverage, depending on he company’s needs.

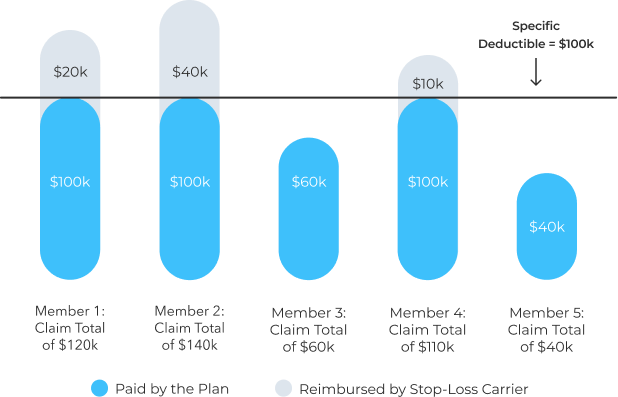

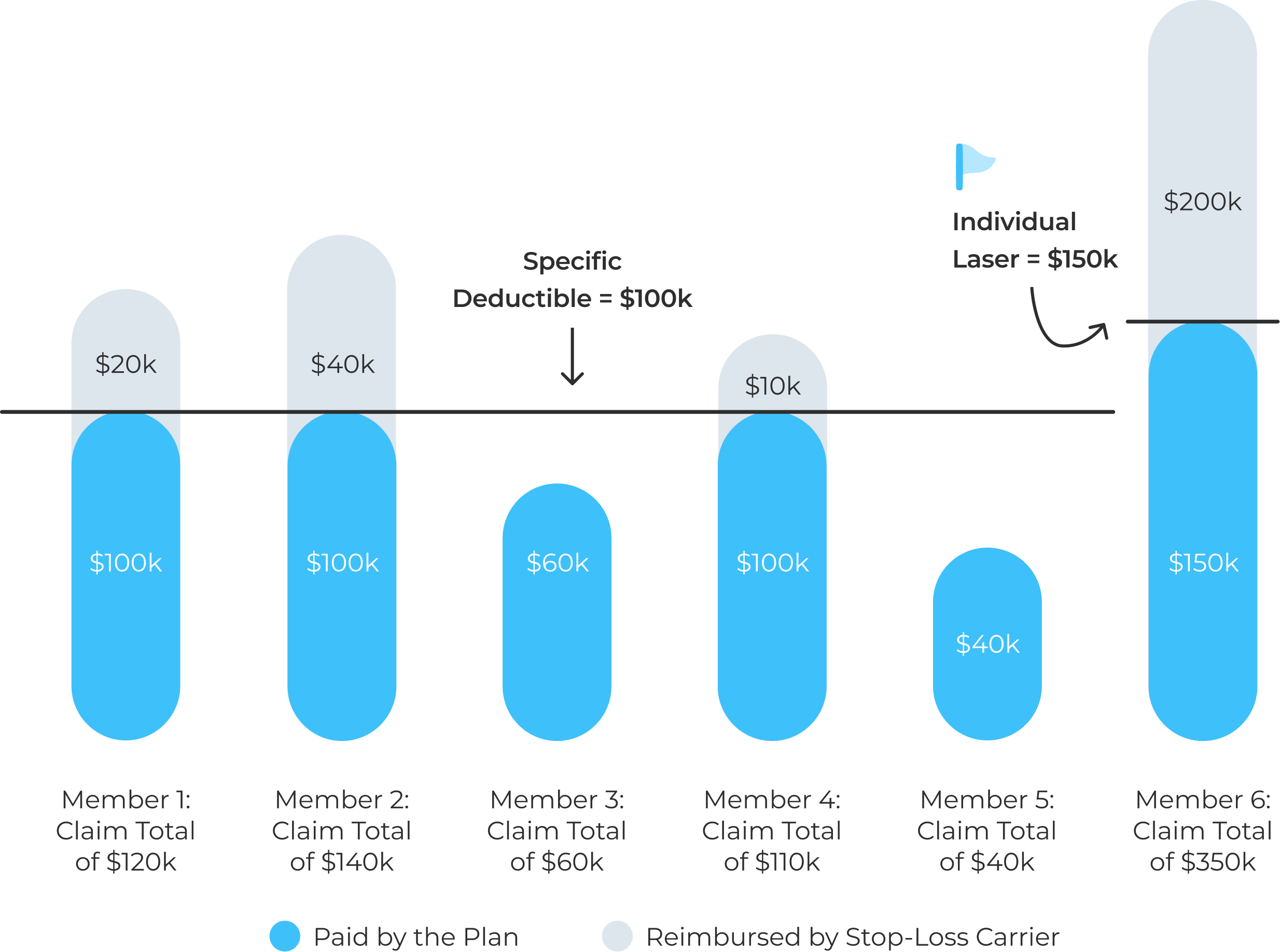

Specific coverage protects your business against the risk of particular claims being too high, setting a spending level for each individual or family on the plan, and reimbursing you if claims rise above that. So, with a contract providing specific coverage of $100,000, you’ll be reimbursed the difference any time an individual member’s claims—including covered family claims—rise above $100,000, just like our earlier example. Specific coverage generally only applies to medical and pharmacy claims.

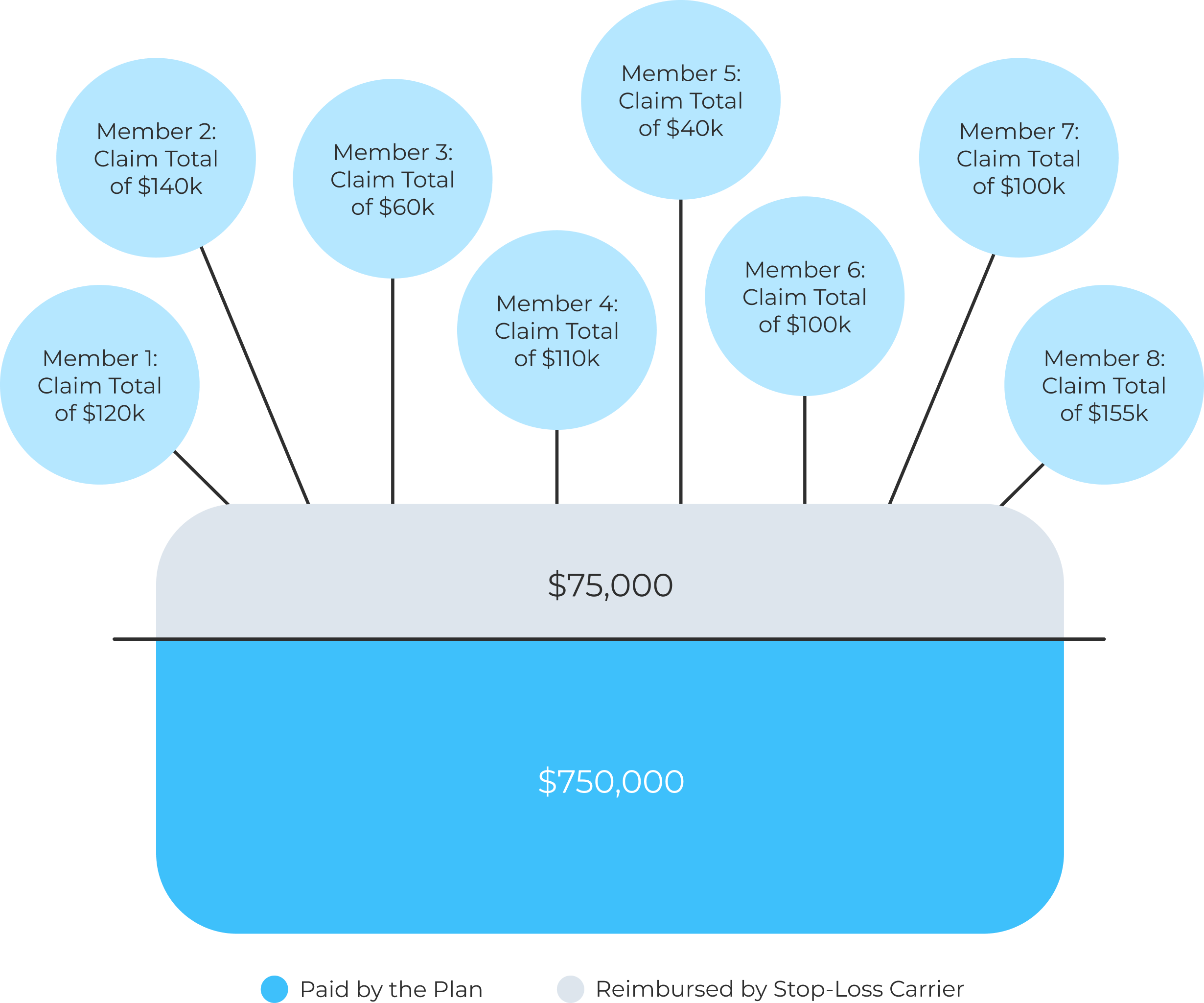

Aggregate coverage, on the other hand, is a spending limit for your entire healthcare plan. It combines all claim cost from all members into one big bucket and reimburses you if spending goes over a limit called the aggregate attachment point. This point is calculated based on projected claim costs, plus a risk corridor to account for unexpected claims. Aggregate coverage typically applies to a broader range of claims—including medical, dental, vision, pharmacy, and short-term disability.

These two types of stop-loss coverage can work together to limit financial risk, but they reimburse different types of claims and never overlap. With specific coverage, you pay claims up to the individual deductible, and then the stop-loss insurer reimburses any excess. With aggregate coverage you pay all claims up to each individual’s deductible across the plan year. If total claims (excluding any amounts already reimbursed under specific coverage) go over the aggregate attachment point, the insurer reimburses the excess. You’re never reimbursed twice for the same dollar of claims. Specific and aggregate coverages complement each other—but always stay in their lanes.

Lasers

Formally known as “individual specific deductibles”, lasers are provisions added to stop-loss contracts to control the risk taken on by the stop-loss insurer. Essentially, a laser sets a higher deductible on an individual with higher expected claims—someones requiring major surgery or dealing with a chronic illness, for example. Returning to our earlier example with specific stop-loss coverage of $100,000, an employee needing regular kidney dialysis might be subject to a laser, bumping their individual specific deductible up to $150,000. That would mean your company needs to pay the additional $50,000 before a reimbursement claim could be filed for the individual. This additional amount is not applied to the aggregate.

Contract Basis

Contract basis describes the way you and your insurer determine which claims are covered by the stop-loss insurance. Contract basis is usually expressed as two numbers representing the date a covered care event can be incurred and when it needs to be paid.

Date incurred indicates when a medical care event actually takes place—the date when a member gets surgery or fills a prescription, for example. Date paid, on the other hand, represents when the insurance policy actually cuts the check to pay for the care that has taken place.

So, for example, a 12/12 contract basis means every claim that is both incurred and paid for over the 12-month period of the contract is covered. However, imagine one of your members had surgery a month before the contract came into effect—in that case, the claim won’t be covered and you won’t be reimbursed, even if you pay for the procedure during the life of the contract.

To avoid problems like these, a variety of different contract bases are available, like 15/12: This would also cover claims incurred in the three-months before the contract, so long as they were paid during the contract’s 12-month period. Another common example is 12/15, covering any claims incurred over 12 months, so long as they are paid within three months of the end of the contract.

At the end of the day, you just want to be sure that your claims will be covered, so it’s important to negotiate contract basis that doesn’t leave you exposed to uninsured periods—remember, that you have the final responsibility to pay members care costs, and without stop-loss, those costs can be arbitrarily high.

Underwriting Medical Stop-Loss Insurance

So, how do stop-loss insurers actually assess your healthcare plan’s risk and set premiums? Like all underwriting, it’s a complicated process, but there are a number of common factors they’ll almost always consider:

Industry

If your industry has higher than average health risks—because it involves physical labor, for instance—your expected claims will likely be higher, meaning higher premiums too.

Demographics

The age, gender and location of your plan members help underwriters predict healthcare usage and costs.

Benefit Design

Giving your plan members more benefits or lowering their deductibles increases the plan’s financial risk, which will be reflected in your premiums.

PPO Network

Depending on the care quality and discounts offered by your provider network, underwriters might expect your claims costs to be higher or lower than average.

Monthly Claims Experience

Recent claims data helps underwriters gauge your ongoing and future risk.

Specific Level

The specific deductible you choose for individual or family coverage directly affects premiums, with lower deductibles leading to higher premiums.

Pre-Certifications and Large Case Management Reports

Evidence of strong cost containment and care management can improve underwriting outcomes and lower premium costs.

Large Claims Reports and Loss Ratio

Your history of high-cost claims and your overall loss ratio indicate the likelihood of future large claims.

Ongoing Claims

Active high-cost or chronic claims increase risk and may affect rates and coverage terms or lead to lasering.

Factors like these are combined using proprietary actuarial models to determine the underlying risk of a plan. From there, underwriters are able to set premiums and decide on appropriate coverage terms for your plan’s stop-loss insurance.

How Your TPA Can Help

As we’ve seen, stop-loss can be a complicated topic, and there are lots of wrinkles to wrap your head around. Fortunately, self-funding companies don’t have to figure out stop-loss on their own—third-party administrators (or TPAs) can help you navigate the stop-loss journey from start to finish, steering you towards the right insurance partners, helping you negotiate contracts, and working with you and the stop-loss insurer to keep things running smoothly year to year.